BYU Marriott

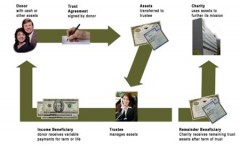

BYU MarriottThe most popular and flexible type of life income plan is a charitable remainder unitrust (CRUT). Cash, securities, real property, or other assets are transferred into the trust. The trustee manages the trust assets and pays you or others you choose a variable income for life or for a term of years. When the trust terminates, the remaining assets in the trust are transferred to the Marriott School.

The typical donor:

- Needs income for life or a specified term of years

- Desires more income as the trust value increases

- Tolerates some investment risk to provide for growth

- Wants to make additional gifts to the trust

- Is between the ages of 55 and 80

Gifts features and benefits:

- Income for life (variable payments)

- Available if needed during life (gift at death)

- Assets transferred to the trust can be reinvested

- Ability to choose the trustee (may be the donor)

- Flexible investment possibilities for the beneficiary

How Do I Make a Gift Using a Charitable

A trust document tailored to your needs is drafted. Your assets are transferred to the trustee you choose. The assets are usually sold by the trustee and reinvested to match your income objectives. You receive variable income for your life or a specified period of years. At your death or the end of the period, the remaining assets are transferred to the charity of your choice.

Before you begin, you need to make sure your financial and legal advisors are part of your gift strategy team. A charitable remainder unitrust can have an impact on other parts of your financial and estate plan. The professional staff at LDS Foundation can assist you and your advisors in the creation of trust documents.

Other Facts You Should Know about a Charitable Remainder Unitrust

The “income tax deduction” you receive from a charitable remainder unitrust is based on an Internal Revenue Service (IRS) formula that considers the ages of the donors and income beneficiaries, the payout of the trust, and an IRS index rate known as the Applicable Federal Rate (AFR). The older you are, the larger your income tax deduction. Generally, if the trust is for a term of years rather than for life, the income tax deduction will be larger. If the present value of the remainder interest equals at least 10% of the value of assets transferred into the trust, the trust will qualify as a charitable remainder unitrust.

There are four types of Charitable Remainder Unitrusts:

- A standard unitrust pays the stated amount from the trust regardless of how much income is earned. The payout is the stated percentage of the trust assets as valued annually

- A net income unitrust pays the stated amount from the trust to the extent of income earned in the trust without invading principal. The payout is the stated percentage of the trust assets as valued annually

- A net income with makeup unitrust pays the stated amount from the trust to the extent of income earned in the trust without invading principal. It has the ability to makeup income in subsequent years if the income earned is less than the stated payout rate

- A flip unitrust is a net income unitrust that “flips” to a standard unitrust when a specified date or event occurs such as a birth, a death, or the sale of a hard-to-market property

The trust provisions you have control of when drafting your charitable remainder unitrust include:

- Choosing a trustee

- Designating the income beneficiaries

- Naming the charitable remainder beneficiaries

- Deciding on a payout rate for the trust

- Determining the frequency of the payments

- Selecting the term of the trust

With a charitable remainder unitrust, certain activities known as “self-dealing” are prohibited. Self-dealing rules prevent a donor who has transferred property to a trust, or a donor’s family, from dealing with the trust. Actions considered to be “dealing” include buying from, selling to, and renting from the trust, and continuing to do business with the trust. The donor, the trustee, members of their families, and entities such as corporations in which they have substantial interests are “disqualified persons” and are prohibited from dealing with a trust that has been a recipient of the donor’s property.

Federal tax law outlines a tier system that determines the taxation of trust income to income beneficiaries of a charitable remainder unitrust. Whether or not all income produced by the trust is distributed to the income beneficiary, the trust pays no income taxes on its earnings as long as it has no unrelated business taxable income (UBTI). An example of UBTI would be debt-financed income. The income to the income beneficiary from the trust is taxed based on the historical pattern of how income in the trust was earned. Income distributions are taxed in the following order:

- Ordinary income

- Capital gain income

- Tax-free income

- Return of principal (corpus)

For example, suppose you transferred a piece of real estate to the trust, and then sold the real estate and reinvested in blue-chip stock that provides both dividend income and capital growth. As income is paid from the trust to you, you would report all income as ordinary income (tier 1) to the extent of all dividend income received into the trust. Only after recognizing all ordinary income would you then report capital gain income (tier 2) from the sale of the real estate. As a general rule, you should assume for planning purposes that trust income will be taxed as ordinary income.