BYU Marriott

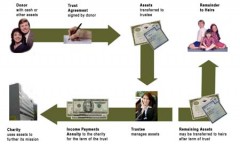

BYU MarriottCharitable lead trusts (CLT) are often viewed as the opposite of a charitable remainder trust. A donor transfers property to the lead trust, which pays a percentage of the value of the trust assets, usually for a term of years, to the Marriott School. At the end of the trust term, the remaining assets in the trust and any growth it has realized are passed to your heirs.

Although there is no income tax deduction when you create a charitable lead trust, your gift or estate tax is greatly discounted and any growth is passed to your heirs gift and estate tax free. It is one of the only transfer devices currently used that can discount the value of the original assets and result in little or no taxes. At the same time, you fulfill your charitable desires.

The typical donor:

- Has a moderate to large taxable estate

- Has given to charities in the past

- Holds assets with growth potential

- Desires to pass certain assets to heirs

Gifts features and benefits:

- Gift and estate tax deduction on the value of assets transferred

- Growth transferred tax free

- Perpetuates a tradition of charitable giving

- Management of assets transferred

A nongrantor charitable lead annuity trust document, the form of charitable lead trust most commonly used, is tailored to your needs by your legal professionals, with the assistance of LDS Foundation’s professional staff. You transfer appropriate assets to the trustee of the charitable lead annuity trust. The assets may be sold or retained, depending on the objectives desired. The trust pays a percentage of the original trust value to the Marriott School. Unlike a charitable remainder trust, a charitable lead annuity trust creates no income tax deduction to you, but the income earned in the trust is not attributed to you. The trust itself is taxed according to trust rates. The trust receives an income tax deduction for the income paid to charity.

The real value of using a charitable lead annuity trust is that the original asset values receive a gift and estate tax deduction based on the value of the income stream given to charity. Excess earnings and growth add to the value of the trust corpus. Each year as the charitable lead annuity trust corpus grows, the percentage paid to the charity represents a smaller percentage of the total trust value. At the end of the trust term, the trust terminates and all the assets in the trust, including growth, are transferred to your heirs without further gift or estate tax.

Before you begin, you should be sure to involve your financial and legal advisors as part of your gift-strategy team. A nongrantor charitable lead annuity trust is only effective as part of an overall financial and estate plan. LDS Foundation’s professional staff can assist you and your advisors in the implementation of a nongrantor charitable lead annuity trust within your overall estate plan.

Other Facts You Should Know about a Charitable Lead Trust

There are two general types of charitable lead trusts—a grantor charitable lead trust and a nongrantor charitable lead trust. Each can be in the form of a unitrust or an annuity trust. A grantor charitable lead trust provides an income tax deduction on its creation to the grantor (donor); however the grantor is taxed on the income paid to the charity. There are limited uses for grantor charitable lead trusts in both the unitrust and annuity variations. Therefore, a majority of estates use a nongrantor charitable lead annuity trust.

A nongrantor charitable lead annuity trust is primarily used in conjunction with an overall estate plan to provide a vehicle that not only greatly reduces the gift and estate tax on the transfer of high growth assets to heirs, but also provides a transfer of the growth tax free. Often you can remain as the trustee during the term of the trust to control management of its assets. Not only is the income from the trust paid to charity and not taxed to you, but it may also replace or enhance outright charitable gifts you wish to make.

The gift and estate tax deduction on the original transfer of assets is an Internal Revenue Service calculation based on the fair market value transferred minus the present value of the income stream to charity. The longer the term, the greater the deduction. Although this method is an attractive way to transfer assets to heirs and make a substantial gift to the Marriott School, it works best when used in estates of approximately $5 million or more.

Like other tools mentioned in this section, the charitable lead trust is most frequently used in conjunction with nongrantor annuity trusts, irrevocable life insurance trusts, Private Foundations or alternate foundations like Donor Advised Funds and Support Organizations, and many other estate-planning vehicles.